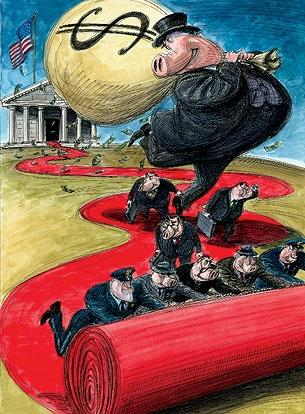

The Banks Purposely and Strategically defaulted on America in 2008...

Ernest Hancock

Website:

www.ernesthancock.com

Date: 12-09-2011

Subject:

Depression

Now it's our time to strategically 'non-default' back on them, by quit paying this week! - Occupy Your Home And Regain Financial Independence

Here is a scenario that my friend Brian recently

experienced.

Four years ago, Brian purchased his family's home for its

ridiculous, phony 'appraisal' of $350K.

Two months ago, Brian still had a burdensome $340,000 left on his

pretender-loan, against his severely upside down home, which, even if he could

sell it at current retail pricing, his home would maybe sell for $210K in today's bank-depressed market, with an

additional $20,000 in 'realty fees' losses.

Upside down and effectively bankrupt, just like Goldman Sachs, AIG, and

Government Motors were in 2008!

Brian researched and discovered he can now 'buy'; this

same-sized house or even floorplan down the street, through several available vacating foreclosures ranging between

$87,000 to $142,000, down his street, or - even in a completely better

neighborhood. Sadly, many of these

foreclosed homes were completely abandoned vacant

by several families too tired, or too uninformed, not to get on Livinglies.wordpress.com,

and occupyourhomes.org/ and

consistently fight against the many

immoral bank wrongs foisted upon them.

BRIAN CLEARLY HAD TWO

OPTIONS:

1. To initially offer

his current pretender servicer bank

$32-55K, and 'settle' for $87K. Then use

a pre-arranged no-qualify PRIVATE 'hard

money' loan from a private lender, to payoff this final 'settlement'

amount. A much smaller $87K legal loan

is now on his house.

or...

2. Brian identified

all the homes being abandoned in his neighborhood or even better

neighborhoods. Brian also watched for

'moving' yard sales. Out of American

moral decency, he tells them all first

about the many opportunities for resisting illegal foreclosure on Living

Lies. If his neighbors still

don't wish to resist corruption, and are moving out of town, back to mommy's

anyway, he then offers these former

neighbors, who are abandoning their pre-foreclosed

home, $1,000 cash for a quit claim

deed for all its alleged 'upside down' equity.

In other words, each of us have to be willing to 'Occupy our Freedoms'

and 'Occupy our home', or lose it to a non- owner bank anyway.

Then Brian moves in this new vacated home and then

immediately purchases and mails off the laymen

letters to their bank, orders the

combo

package for pre-discovery chain of title, then sues their bank(s) for quiet title, and then

offers to aggressively settle for

$56K, then actually ends up settling

with their bank for $87K with $3,000

down, with that bank causing 'rewriting' by replacing the null note and deed of

trust for $84K new note @2% within a tax-free court settlement, to wipe away

all the bank's civil illegalities. As

an intricate part of this 'settlement', the bank carries the alleged 'balance'

of this new note, no real qualifying, no silly, needless 'asset'

disclosures. Brian also demands this bank

buy him new title insurance (particularly against any pretender recorded

encumbrances)1; a court-settlement-agreed to NO deficiency; as well

as recorded bank indemnification of Brian from any other claims from all comers,

forever.

BRIAN'S BIG RESULT:

Either way, whether within his old home, his new one, or

both, Brian has just wiped off $263K of principle debt OFF his life, which AT

INTEREST, over the next 30 years, his $263K would

have been about triple, or about $650,000

cash less to the pretender bank!

By saving $650,000 in this

two-step, strategic non-default, Brian

has just taken 20 years off his working life, even during one of the

greatest modern American depressions.

Brian can now pay off his new small $84K note off in about 10 lousy

years! Then, during the next 20

following years, Brian puts his entire former house payment amounts, into his hard-metal2

money retirement and new family adventures, and starts spending masses of more

fun time with his precious kids and smiling wifey.

Brian will have to earn wayless from now on, with his wife now

able to completely quit work and properly raise their kids - so now Brian will

now also be paying about $200K less

in Federal Reserve-interest, ie. 'income taxes' as well over those 30 years too3! Brian

has now decided to take his family on two

major 30-day vacations each year, and get his kids better private or home

schooling with all this extra time

and money4... His money. His

time.

ALL JUST because Brian decided to

"strategically non-default" on his current pretender lender -

similarly as these same banks did to his countrymen and America in 2008!

To assist aggressive pre-settlement with the

scared-to-get-caught bank, Brian ordered the laymen

letters from LivingLies Store, specifically modified to that lender and

sent them to both his current bank, as well as, to the bank on his new

quitclaimed home. This gave both banks

many more valid reasons to settle, because each bank wanted to cover-up its

foreclosure and assignment frauds, and keep the OCC from finding out about

their continuing, non-stop violations of the OCC's April 2011 Consent Orders!

This entire time, even though Brian had quit paying both of

his pretender house 'payments', Brian was in "non-default", because

the pretender servicer bank was not

the real party in interest; and further, the loan's note and mortgage/deed of

trust were separated from each other, when securitized (tax-free) years ago,

making them null, per the often-cited

U.S. Supreme Court decision, Carpenter v.

Longan.5

The servicing bank wisely wanted to cover-up this nullity,

and they had already received yet another a taxpayer bailout6 for

all the investor losses they caused anyway, which further flagrantly violated

the 'Collateral Source' rule against Brian.

The ugly burden of American's financial-crime's depression,

now moved from Brian's family, over to the soulless 'United Banks of

America', where they belonged!

A win-win situation for Brian and America!

These rotten banks defaulted on our America in 2008, and

then received $16 Trillion+ in taxpayer-backed bailouts secured by 'taxes' upon

Brian's three jobs.

In contrast, like Brian, let's now mimic the bank's cunning

example - against them, and

strategically 'non-default' on them, by not paying them anymore, when we are

severely upside down.

We the People are too big to fail, not these Ponzi banks and

their fiat money.

As free-enterprise Americans, "Our word is good as our

bond". So, although we still pay

all our real debts that we borrow

from friends and people who actually

worked for the money they lent us

- we cannot, and should not, pay the bank's Ponzi-scheme pretender

non-worked-for created-out-of-thin-air 'debts' - 14,000 times bigger than

Bernie Madoff's schemes, to the tune of $705,000,000,000,000.00 Dollars3. Which is also 14 times bigger than the

world's entire money supply. Mission

impossible! Why even try?

Like Brian, quit paying, when you can save hundreds of

thousands of dollars in principle and interest over these next 30 years of your

life.

Get a new life. ... Time for your family, friends, and your

young dreams!

Strategically non-default!

BRIAN'S STRATEGIC,

PRE-NON-DEFAULT CHECKLIST: ĂĽ 1-20

Like Brian, are you 'upside down' more than a few thousand

dollars? Is there little or no

foreclosure deficiency in your state on your primary home? Then like Brian, it may make great sense to:

Sell

or transfer most of your non-exempt other assets like the congressmen, to

irrevocable trust(s) for the kids as beneficiaries when you pass. Take out all but a few $100 cash out of

banks and deposit accounts like CD's, 401K's, stocks, etc, so they can't

be electronically plucked from anyone.

Become an expert about your

state's thresholds of

non-deficiency, debt exemptions, and most importantly, your state's homestead exemption amounts. Get on the internet and study your

state. Quickly become an expert at these numbers, like the

banks, and able to repeat these in your sleep.

Have

your lawyer or yourself purchase and send the laymen

letters to your banks. Put the

pretender servicer banks on notice, that you are onto their wrongful loan

servicing, foreclosure frauds, assignment frauds, etc. Brian believes every loan negotiation

with a bank should be done from an very aggressive legal-mitigation position for the pretender

bank. The bank needs to know they

done real wrong, and you now know it.

Greatly lowball bid the foreclosures in

neighborhoods you would like to live in. Start bids very low at

perhaps 20% of current

foreclosure value, say about $32K, then perhaps work up to $87K, in what was

once an old $350K neighborhood.

If

your credit is still good, use your current home as a new rental for

qualification, before you quit paying pretender payments on it. If your credit is bad, no problem. Skip this minor and unnecessary step #5.

If

your credit is not good, so what. Pre-arrange for a PRIVATE asset-only-based 'hard money' loan to accomplish the same lowball purchase, with a

considerably temporary higher interest rate, until you can refinance it

after two to three years. Be wise and avoid prepayment penalties that

persist over a year and other weird quirks. Unlike the last time you signed, read

and understand all of the fine

print.

Complete

purchase - and prepare to move in your new same, or even better home!

Then,

quit paying your pretender lender on your old home, and save all the rent7 money for your future in gold and silver

coin. (Boycott the banks, don't put

it in there or they may sneakily attempt to back-charge or confiscate your

money, through their account-agreement's fine print).

Study

and use LivingLies strategies as a part-time

job, to prolong the pretender's bank's fear of doing wrongful

foreclosure. Keep collecting

rents. Store all your rent

recoupment of your down payments and other misallocated payments in gold

and silver coins. Don't let the

bank get at them. Get good at

securely hiding them in various places, like your smart great-grandfather

did in the 1929 Depression, against his era's banking and political

evils. (same ones).

Eventually

sue the pretenders for quiet title on your old home for nullity, or let

your old home go to a deserving needy homeless family for a few months,

under the Protecting Tenants at Foreclosure Act of 2009.

Sit

down with your family and strategize your new financial life together.

Rebuild

your closeness and dreams. As some

wise books say: "Make a Memory" with them! Lots of them - You have the time and

money now8.

Get

better schooling, even if you have to do it yourself. Teach, and keep your kids out of the

drafts for unconstitutional foreign wars, paid for with all this phony bank interest. Your kids and grandkids are worth more

than every 'leader's' temporal, turf-dominance power trips.

Buy

months of extra food for any future grocery store disruptions.

Teach your understanding, good-quality

friends how to do the same!

With this extra

time, let's all work to cancel

ALL bank residential mortgages in America for nullity and fraud. This effort is

also a major non-party political movement to preserve America by preserving families stability, by preserving their

real financial independence - completely divorced and independent of the

phony fiat financial system.3 With this extra

time, let's all work to cancel

ALL bank residential mortgages in America for nullity and fraud. This effort is

also a major non-party political movement to preserve America by preserving families stability, by preserving their

real financial independence - completely divorced and independent of the

phony fiat financial system.3

Let's

also all work to completely replace our worthless fiat, Ponzi,

inflationary paper money, with gold and silver coin, as our Constitution

demands. Real slavery will never end, until we do.

Let's

rebuild our American character, financial independence, and fun times

together.

Let's

then rebuild our American dream and liberty, as out founding fathers

created, not as 'interpreted' by the gird.

We

have nothing to lose, but our chains...

...and about 60 great vacations!

Print and reread this a few times over days, until you really start to understand it.

Freedom is not free.

Implementing Brian's strategy hard this year, will save

many of you 20-Years of Interest and Hard Work

Indict the Big Bankers With Your New-Found Financial

Freedom and Activism Today

_________________________

1 Brian's new home-title here is actually fully valid,

because the pre-foreclosure actual

recorded owner quit claimed to Brian

for $1,000 consideration. Only

unresolved or phony liens of pretender banks are to be the resolved issue from

this point forward.

2 Precious Metals are real gold and real silver in

hand. Do not get lazy, insecure, or greedy, and buy 'paper' gold. It is estimated there is a least 20 times of

phony bank 'paper' gold, than that which actually mined over entire history of

the earth. Take physical possession

simultaneously at purchase with green cash, and squirrel away within many

separate well-thought out holes. Do not store in banks. Thereby

resist later confiscation by corrupt political fads such as was done in

1934. http://www.trendsresearch.com/SubscriberArea/pt-1-2-gerald-celente-infowars-nightly-news-28-nov-2011

3 And you wonder

why the federal and most state governments are recklessly, desperately, and

artificially keeping 'home prices up' and covering

up these bank crimes across the nation and world, over the last four years,

even though they've read and catalogued the masses of banker crimes on LivingLies

everyday! They all know what is going on

in every detail. They are all a part of it, so the scam and

its huge revenue schemes from Brian's three jobs, won't lessen, till he

discovers his grave around age 85. Most

of the government, all of the Federal Reserve, Goldman Sachs, AIG, City of

London, Bohemian Grove, and all medium+-sized banks fully participate in this

financial criminal cover-up, day after day.

For you to attempt to pay off

their phony $705 Trillion in Derivatives bearing interest, you and your kids

will work 10,000 generations to pay it off!

Contrary to the history books, slavery has yet to end in this world.

The beginning of the 21st Century unfortunately is one of slavery, if

everyone doesn't pull a 'Brian'-type strategic non-default on them. All the work product of this entire world was

fraudulently and effectively bought' without

one-hour's real work, including all of your family's generations of toil by

writing the dollars to buy it on a piece of paper! Their debt is phony. Boycott all big banks and all their octopus's

tentacles, political and business.

5 Carpenter v.

Longan, 83

U.S. 271, at 274 (1872). “The note and mortgage are inseparable; the former as essential, the latter as an

incident. An assignment of the note

carries the mortgage with it, while an assignment of the latter alone is

a nullity”. This major

black letter mortgage case has been used extensively by modern courts over the

last three years. Null means void.

7 Rents - you cannot pay rents to a non-real party in

interest pretender lender. They have no

legitimate claim to the mortgage contract

language out of a null mortgage/deed

of trust document. Summarily kick out

all your renters who attempt to misuse the bank's devious threat letters and

visits, not to pay you. Disclose the

unresolved dispute with the bank in your leases. Throughout the foreclosure process, you still

have at least full possessory

ownership, that you can rent out during

this possessory interest, even past foreclosure. The pretender bank can finally disclose the

real party in interest so you can see if their note and mortgage were separated

per Carpenter v. Longan. This would be the only party with a claim to

the Mortgage contract language.

'Possessory' legal definition at:

8 "Brian"

and his wife now hang out with her kids regularly, "making

memories". Her kids are still

wondering how they escaped that windowless 12-year prison. Brian's wife now

donates 6 hours on various weeks to her favorite charity, as she no longer has to work. She also helps out LivingLies.wordpress.com,

emailing it to all her friends, and volunteers for other real freedom causes

with some of her free time! She even had

time to make a small backyard garden for self-reliance. Mission accomplished!

___

Closely-related videos and

info:

___

Note - Do NOT try Brian's

approach on private, non-securitized,

or non bank-fractional-reserve mortgages.

For free enterprise capitalism

to survive (in contrast to misnamed, monopolistic 'capitalism'), our private

word needs to be good as our bond,- If

in trouble, attempt to settle or bankrupt honorably

with innocent non-federal-reserve private creditors. Save America's non-bank-tied markets from

corruption and default.

Print this

article, save in your Documents, and retain for regular instructional

reference. You can do it!

Enjoy this article?!? Please take 2 minutes and email it, or its

link, to several hungry friends.

'Copyright 2011. All Rights Reserved.'

===========================

Lobbyists Have Wrote US Laws That Have Set Up The Biggest Robbery In World History

You read a lot about the enormous

transnational casino called "derivatives" on FreedomsPhoenix, but did

you know that the banks invented a special "Chapter 15" bankruptcy

process in 2005 that is only for "international financial institutions",

and allows them to pay off the derivative gambling debts FIRST before

even depositors?

|