News Link • Corruption

The Greatest Theft in Human History! The Banks and Government Are Stealing $3.5 Million...

• Daily News from the Art of Liberty FoundationHow the fractional reserve banking system, government taxation, and a manipulated inflation number combine to extract more than a full lifetime of earnings from every American worker

How the fractional reserve banking system, government taxation, and a manipulated inflation number combine to extract more than a full lifetime of earnings from every American worker — confirmed by four independent AI systems.

By Etienne de la Boetie2

Founder, Art of Liberty Foundation

With research assistance from Anthropic's Claude, xAI's Grok, Google's Gemini, and OpenAI's GPT – Full Analysis Available at ArtOfLiberty.org/Inflation

Let's start with a number: $3,520,000.

That is the amount the median American worker earning $60,000 per year will lose — over a 40-year career and 20-year retirement — to the fractional reserve banking system, government taxation, and Social Security benefit manipulation. Combined, these mechanisms extract 147% of gross lifetime earnings. More than you will ever earn. The system doesn't just take your money — it takes money you haven't earned yet, your purchasing power vs. an honest monetary system, and then rips you off in retirement by underpaying you what you are really owed in Social Security benefits.

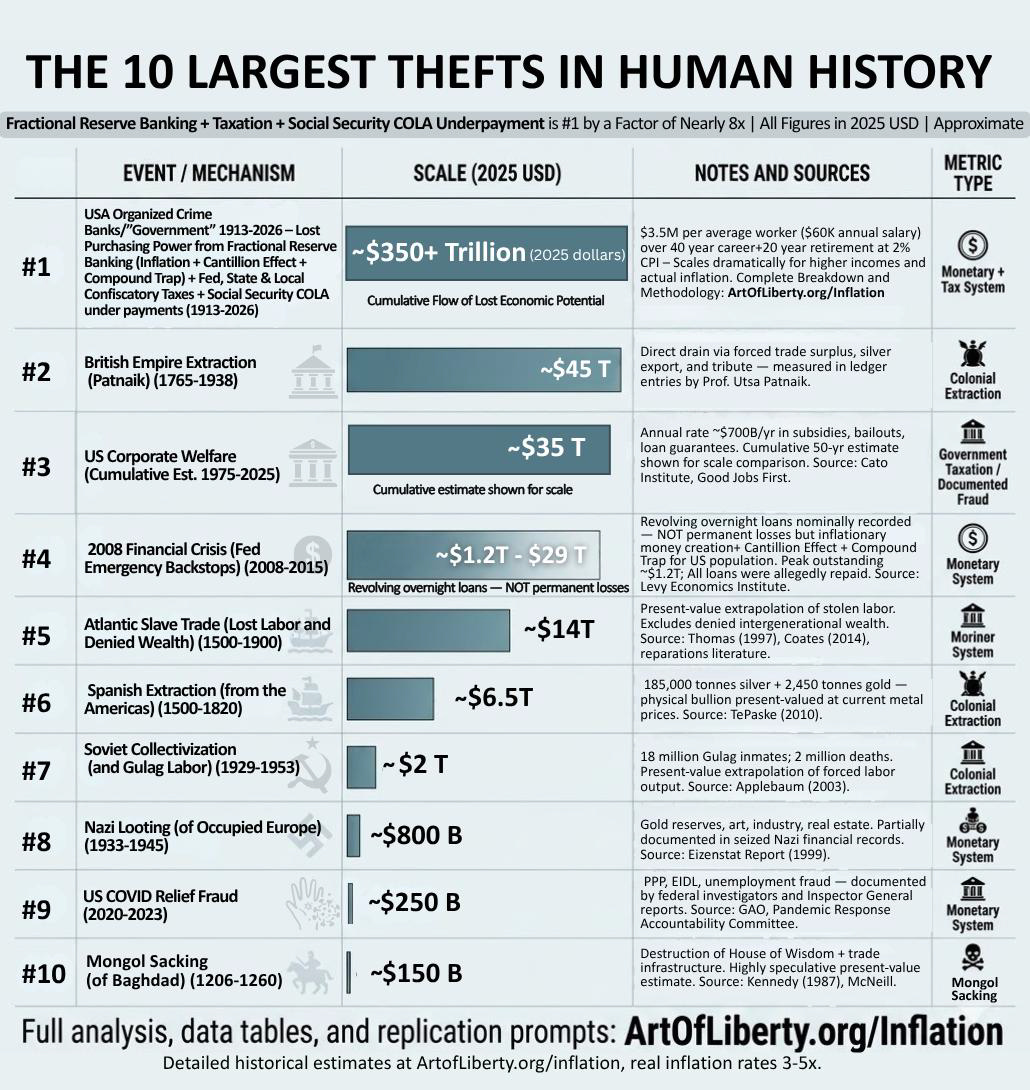

This is not a political opinion. It is not a conspiracy theory. It is an accounting — calculated independently by four separate AI systems using audited primary-source data from the FDIC, the Federal Reserve, the BLS, and the GAO. When Claude, Grok, Gemini, and GPT-5.2 all produce the same order of magnitude without coordination, the pattern is not noise. It's signal.

Today, the Art of Liberty Foundation is releasing The Greatest Theft in Human History — the most comprehensive public accounting of monetary extraction ever attempted. Here's what we found.

The Number That Should End the Conversation

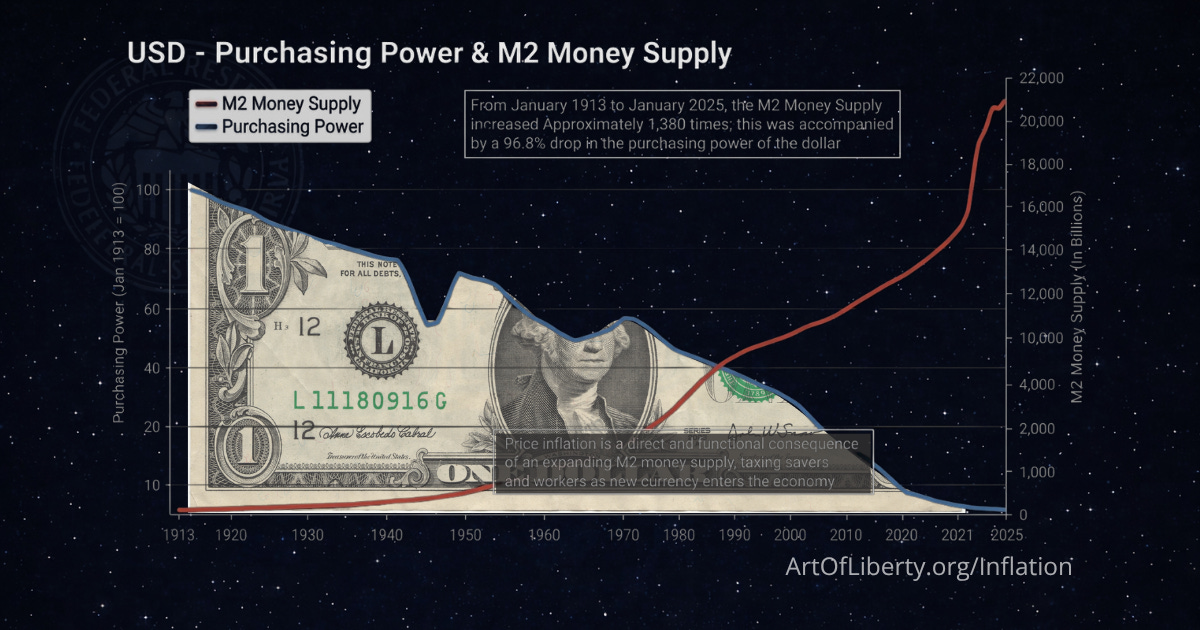

The dollar has lost 97% of its purchasing power since the Federal Reserve was created in 1913. That's not an estimate. That's from the Bureau of Labor Statistics' own CPI Calculator.

During that same period, the M2 money supply expanded approximately 1,380 times— from roughly $25 billion to $21.5 trillion. Real GDP grew approximately 100 times. The gap — 43 times more money than economic output — represents purchasing power transferred from everyone who holds dollars to those who created the new ones.

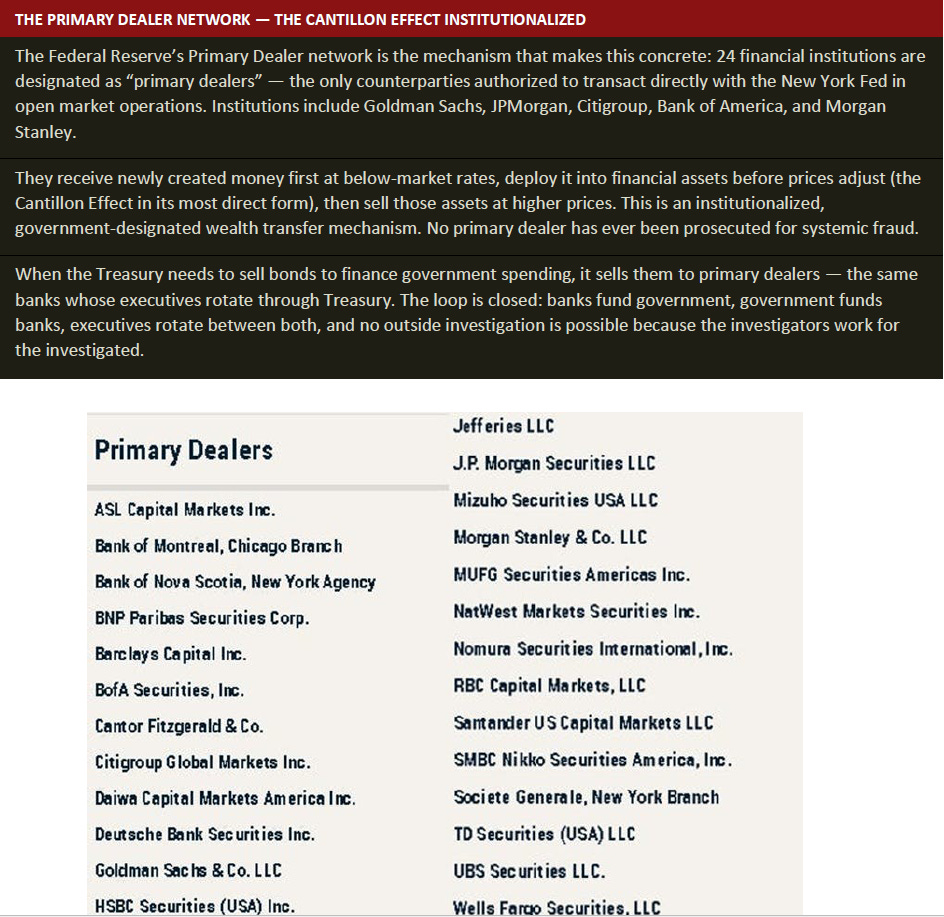

Those new dollars were not created democratically. They were created by banks — private institutions that generate money by typing numbers into computers when making loans — and injected into the economy through a network of 24 "Primary Dealers" who get access to newly created money first, before prices adjust. By the time that money reaches your paycheck, prices have already risen.

This is the Cantillon Effect: a 300-year-old observation that new money doesn't enter the economy neutrally. It enriches those closest to its creation and impoverishes those furthest from it. In 2024, U.S. banks earned $268 billion in net income — confirmed by FDIC audited data. Over the full period since 1913, cumulative bank profits run to an estimated $15–25 trillion in today's dollars.

"Every dollar the banking system extracts is a dollar that, under honest money, would have gone to the person who earned it."

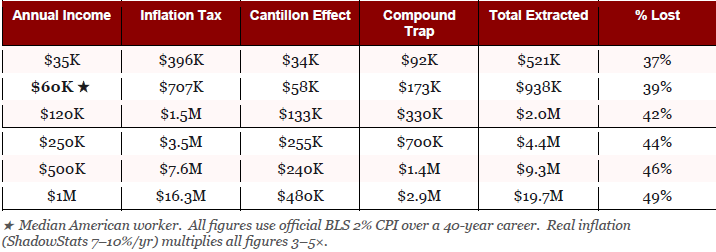

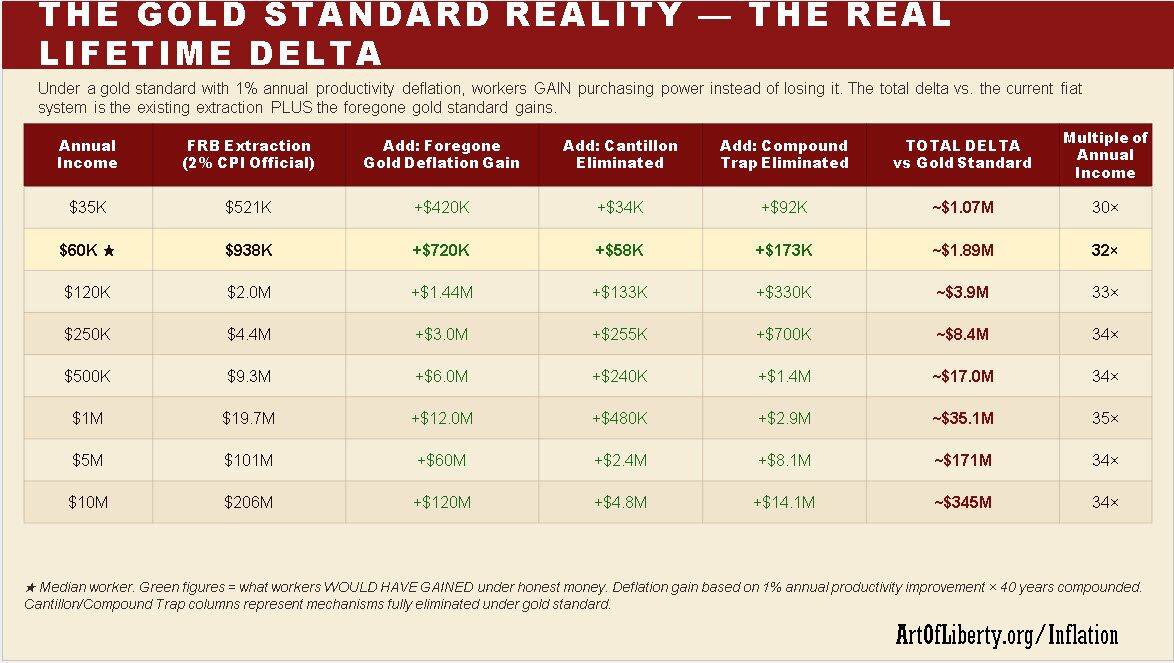

Your Missing Millions

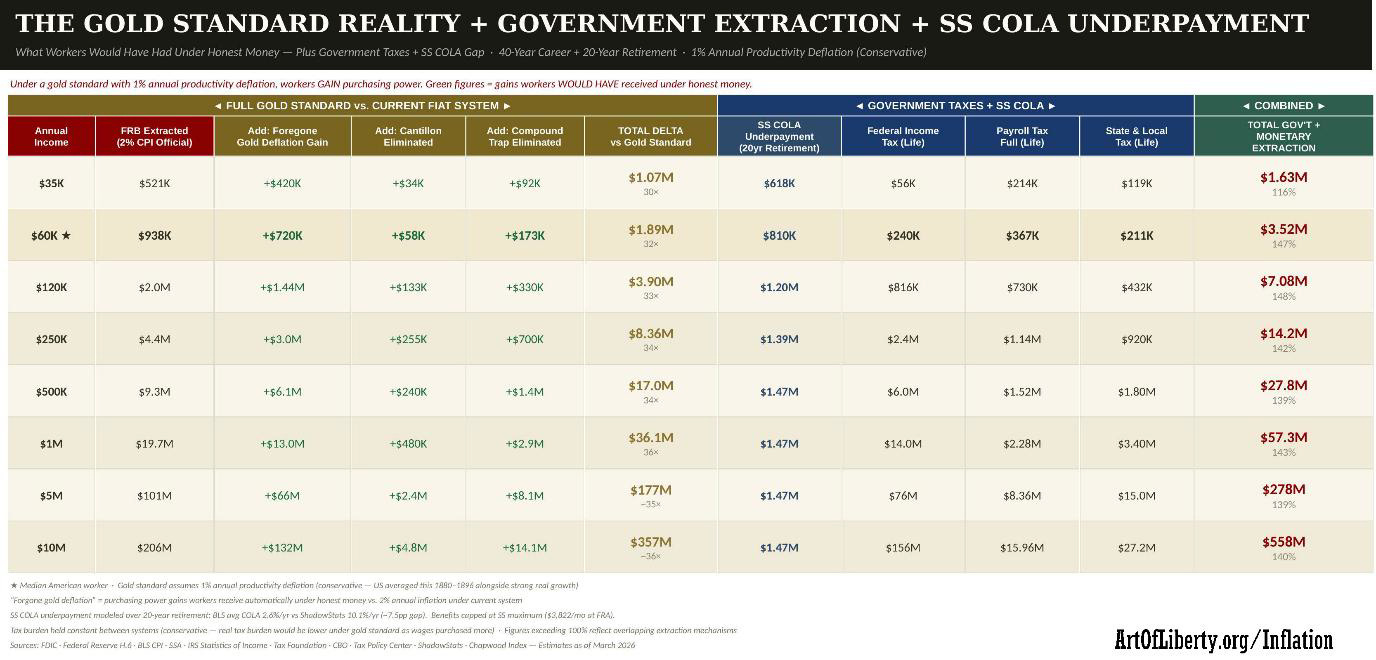

Here is what the extraction looks like, by income level, over a 40-year career using the Fed's own conservative 2% inflation target:

Understanding the Cantillon Effect & The Compound Trap

The purchasing power that evaporates under inflation is only one aspect of the theft of fractional reserve banking. The system also extracts using the aforementioned Cantillon Effect where the banks (Primary Dealers) who receive the new money created out of thin air are able to capture the maximum purchasing power of that money which is reduced considerably once it reaches the average worker.

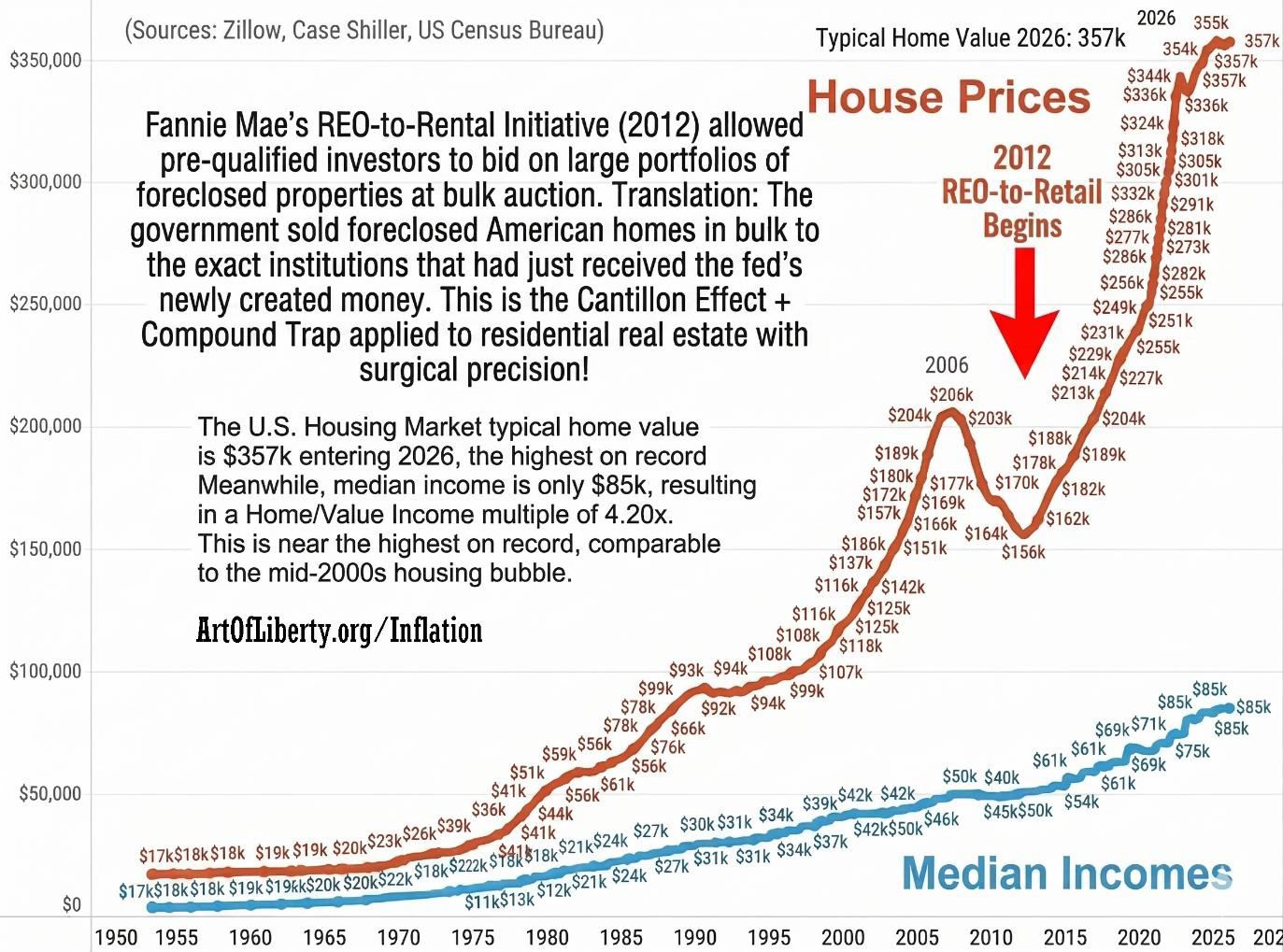

Banks and their borrowers receive new money FIRST, before prices adjust. They buy at pre-inflation prices; workers receive wages last, at post-inflation prices. This is a directional wealth transfer, not neutral dilution. Think about the 500,000+ single-family homes that private equity has bought since 2012, driving up costs for everyone. The institutional single-family rental (SFR) industry is the Cantillon Effect made flesh — in the one asset class workers historically used to escape inflation.

The Global Financial Crisis of 2008 produced roughly 3.8 million foreclosures by 2010, with 7+ million eventual foreclosures by 2014. Median home prices dropped 33%. The people losing those homes couldn't get credit to buy them back because mortgage standards had tightened. The institutions that received the Fed's QE money could.

The key government catalyst: Fannie Mae's REO-to-Rental Initiative (2012) allowed pre-qualified investors to bid on large portfolios of foreclosed properties at bulk auction — an arrangement that individual families physically could not participate in. The government sold foreclosed American homes in bulk to the exact institutions that had just received the Fed's newly created money.

By 2024, institutional investors owned approximately 450,000 single-family rental units (GAO-24-106643). The Philadelphia Fed documented that institutional investors raise rents 60% faster than individual landlords.

The same cheap money that erodes your wages also inflates the assets you can't afford to own — and the institutions that received that money first are now your landlord.

The Compound Trap

The Compound Trap is the mechanism by which the inflation created by fractional reserve banking forces workers to borrow at interest — from the very institutions that created the inflation — to afford assets whose prices have been inflated by the money creation process itself.

Examples:

Housing: A home that cost $25,000 in 1971 costs $400,000+ today — not because the home is 16x better, but because the money supply expanded 1,380x while GDP grew only ~100x. The worker must borrow $320,000 at interest from a bank that created the money out of thin air. Over 30 years at 7%, they pay $446,000 in interest alone — more than the house. The bank risked nothing.

Education: College tuition has risen 1,200% since 1980, far outpacing general inflation. Students borrow $37,000 on average (and often much more) to purchase credentials in a labor market that has not kept pace with credential inflation. The loans are made in bank-created money; the interest is real.

Healthcare and Consumer Debt: Medical costs, auto loans, and credit card balances all compound the trap. Each dollar borrowed is a dollar that was created by the banking system, and each dollar of interest is a transfer from the worker to the bank that created the principal from nothing.

The median worker at $60,000/year pays approximately $173,000 in compound trap costs over a 40-year career — in mortgage interest, student loan interest, and consumer debt interest — all on money that was created out of thin air.

Under alternative inflation indexes (ShadowStats/Chapwood 7–10%), these figures multiply 3–5x.

The Monopoly Government's Confiscatory Taxes: $818,000 from the Median Worker Adds to the Extraction

Federal, state, and local governments extract approximately $818,000 from the median worker earning $60,000 over a 40-year career: $240,000 in federal income taxes, $367,000 in payroll taxes (the full economic burden, including the employer share that would otherwise be wages), and $211,000 in state and local taxes. For the $250K earner, the figure reaches $4.46 million. For the $1M earner, $19.7 million.

The Honest Acknowledgment: You Received Some Services

Unlike the fractional reserve banking extraction — where the wealth transfer produces no benefit whatsoever for the worker — government taxation does fund services that people use. Roads, courts, national defense, law enforcement, fire protection, public schools, Social Security, Medicare, and Medicaid are real services delivered to real people. Our analysis does not pretend otherwise.

But acknowledging that services exist is not the same as accepting that the price was fair, the delivery was efficient, or the arrangement was voluntary.

Three structural problems make the tax extraction far more damaging than it appears:

Problem 1: The Waste Is Staggering

The GAO's own auditors — not libertarian critics, but the government's internal watchdog — estimated that the federal government loses between $233 billion and $521 billion annually to fraud alone (U.S. GAO, based on fiscal years 2018–2022). In FY 2024, agencies reported $162 billion in improper payments across 68 programs, with 84% being overpayments (U.S. GAO). Since FY 2003, cumulative improper payment estimates have totaled approximately $2.8 trillion (U.S. GAO) — and the GAO acknowledges this is a substantial undercount because many susceptible programs don't report at all.

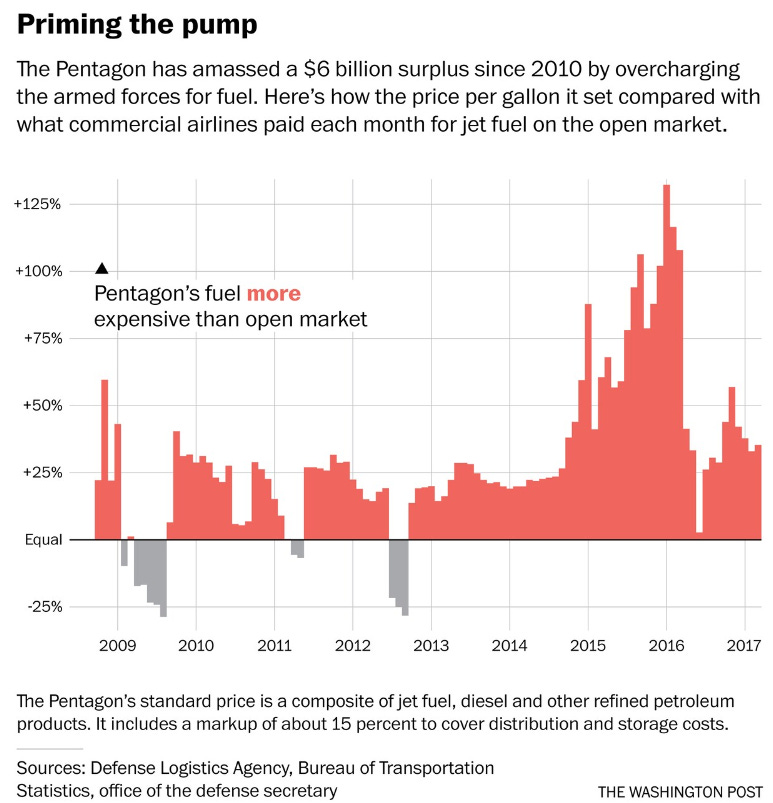

In a scandal that came to be known as the Pentagon's Bishops Fund scandal, the Department of Defense was caught buying fuel in bulk and then reselling it to the individual armed services at a cost significantly higher than if they services just bought fuel on the open market. They took the "profits" and put them into a slush fund.

That means the federal government admits to losing roughly $162–$521 billion per year to waste, fraud, and improper payments. The median worker's $240,000 in lifetime federal income taxes includes their proportional share of this waste: approximately $30,000–$80,000 over a career that went to payments the government itself says should never have been made.

Problem 2: Monopoly Pricing

Government services operate as coercive monopolies — you pay whether you use them or not, and you cannot choose a competing provider. Economic theory and empirical evidence consistently show that monopoly providers charge more and deliver less than competitive alternatives.

Private sector administrative overhead runs 5–17% depending on the industry; the federal government's effective overhead — including compliance costs imposed on citizens and businesses — has been estimated at 20–35% when hidden regulatory burdens are included.

A conservative estimate: if the services currently provided by government were delivered through competitive markets at private-sector efficiency levels, the cost savings would be 30–50% on the service-delivery components — representing roughly $250,000–$400,000 of the median worker's lifetime tax burden that purchased bureaucratic overhead, waste, and monopoly pricing rather than actual services.

Problem 3: The Seen and the Unseen

The most devastating cost of taxation is not what the government spent badly — it's what the economy never produced. Every dollar extracted in taxes is a dollar that was not saved, invested, or spent by the person who earned it. The cumulative effect of removing $818,000 from the median worker's lifetime economic activity — and trillions from the economy as a whole — is reduced capital formation, less entrepreneurship, fewer innovations, and slower productivity growth.

Economists call this the "deadweight loss" of taxation — the economic activity that is destroyed, not merely transferred. Estimates of the deadweight loss range from $0.20 to $0.50 per dollar of tax revenue raised, meaning that for every dollar the government collects, an additional $0.20–$0.50 in economic value is destroyed in the process. Applied to the median worker's $818,000 lifetime tax burden, this represents an additional $164,000–$409,000 in economic value that simply ceased to exist — jobs not created, businesses not started, innovations not pursued, and compounding growth never realized.

Under a voluntaryist free-market alternative, the services people actually want — roads, dispute resolution, security, education, healthcare, retirement savings — would be provided by competing firms, mutual aid societies, and voluntary associations at market prices, with the discipline of consumer choice replacing the inertia of monopoly.

Fraternal societies and mutual aid associations provided healthcare insurance, disability insurance, pensions, and other safety net services before they were crowded out by the monopoly "free" services mandated by "government." The various organizations competed vigorously with each other to see who could provide better benefits at the most cost-effective prices.

Historical examples are not hypothetical: private roads, private courts (arbitration handles more commercial disputes than government courts today), private schools (which educate at roughly 50–70% of the per-pupil cost of public schools), and fraternal societies that provided healthcare and life insurance to working-class Americans before government programs crowded them out in the mid-20th century.

The $818,000 is not the price of civilization. It is the price of monopoly — and the monopolist has $2.8 trillion in admitted payment errors to show for it.

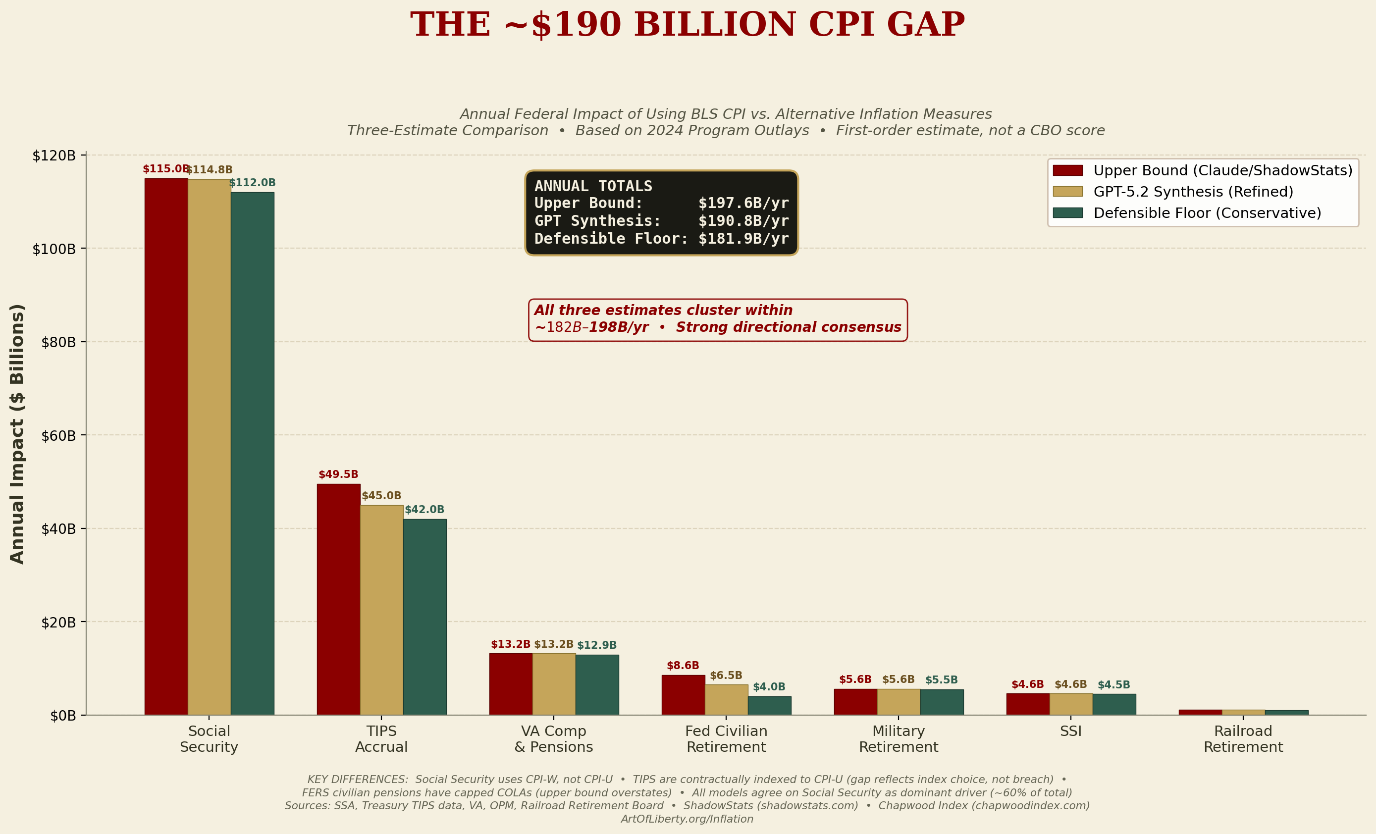

The Government's $190 Billion Incentive to Lie About the Actual Rate of Inflation to Steal Grandma's Social Security

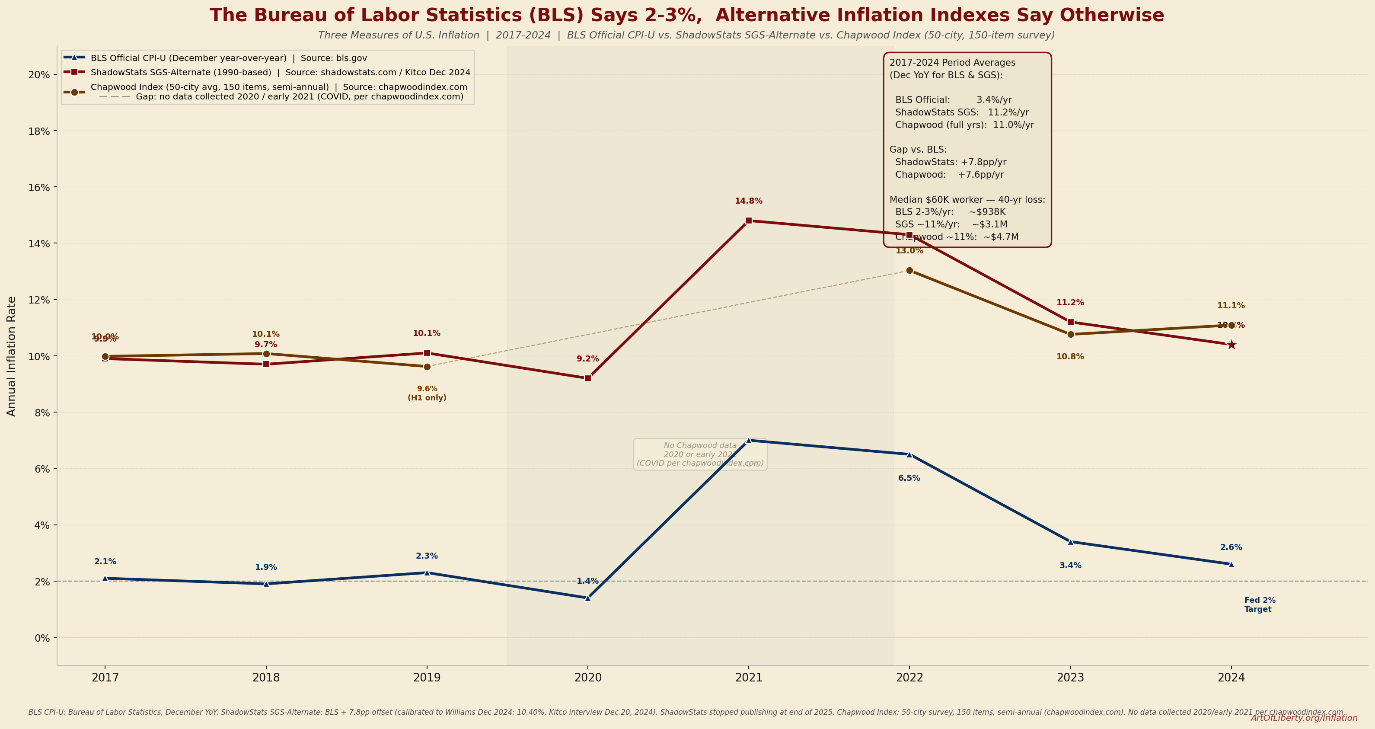

The BLS's "official" inflation number drives Social Security COLAs, federal pension adjustments, military retirement, TIPS bond yields, and more. If that number is systematically low, the government saves money — at the direct expense of retirees and veterans.

Our analysis — confirmed independently by all four AI models — finds that using real inflation rates (as measured by the ShadowStats SGS-Alternate or the Chapwood Index, both of which show 9–11%/yr versus the BLS's 2–3%) would increase federal CPI-linked obligations by approximately $182–198 billion per year. Social Security alone accounts for roughly $112–115 billion of that gap.

The mechanism is elegant in its dishonesty. The Social Security Act requires COLAs to be based on the CPI-W "as published by the Bureau of Labor Statistics." The law doesn't specify how the BLS calculates it. So when the BLS introduced Owner's Equivalent Rent (1983), geometric mean weighting (1999), hedonic adjustments, and substitution bias — each of which independently lowers measured inflation — it automatically reduced every COLA payment in the federal budget without a single Congressional vote.

The compounding effect is devastating. A retiree who began collecting Social Security in 2004 receives approximately $2,032/month today under BLS-based COLAs. Under ShadowStats-level adjustments applied to the same starting benefit, they would receive approximately $4,500–5,000/month. The cumulative lifetime underpayment for a single retiree exceeds $200,000 — and the median worker retiring today will have a 20-year retirement COLA shortfall of approximately $810,000.

The two numbers aren't contradictory — they're the same mechanism at two different scales. The $200,000 is a historical example anchored to a real retiree who started collecting in 2004 at the then-average benefit of $922/month. The $810,000 is a forward projection for today's median worker retiring at roughly $2,100/month — more than double that baseline.

Since the annual COLA shortfall is a percentage gap applied to the monthly benefit, a higher starting benefit produces a proportionally larger dollar shortfall every year. That shortfall then compounds geometrically over 20 years because each year's understated COLA reduces the base from which the next year's adjustment is calculated. Same theft, two different scales.

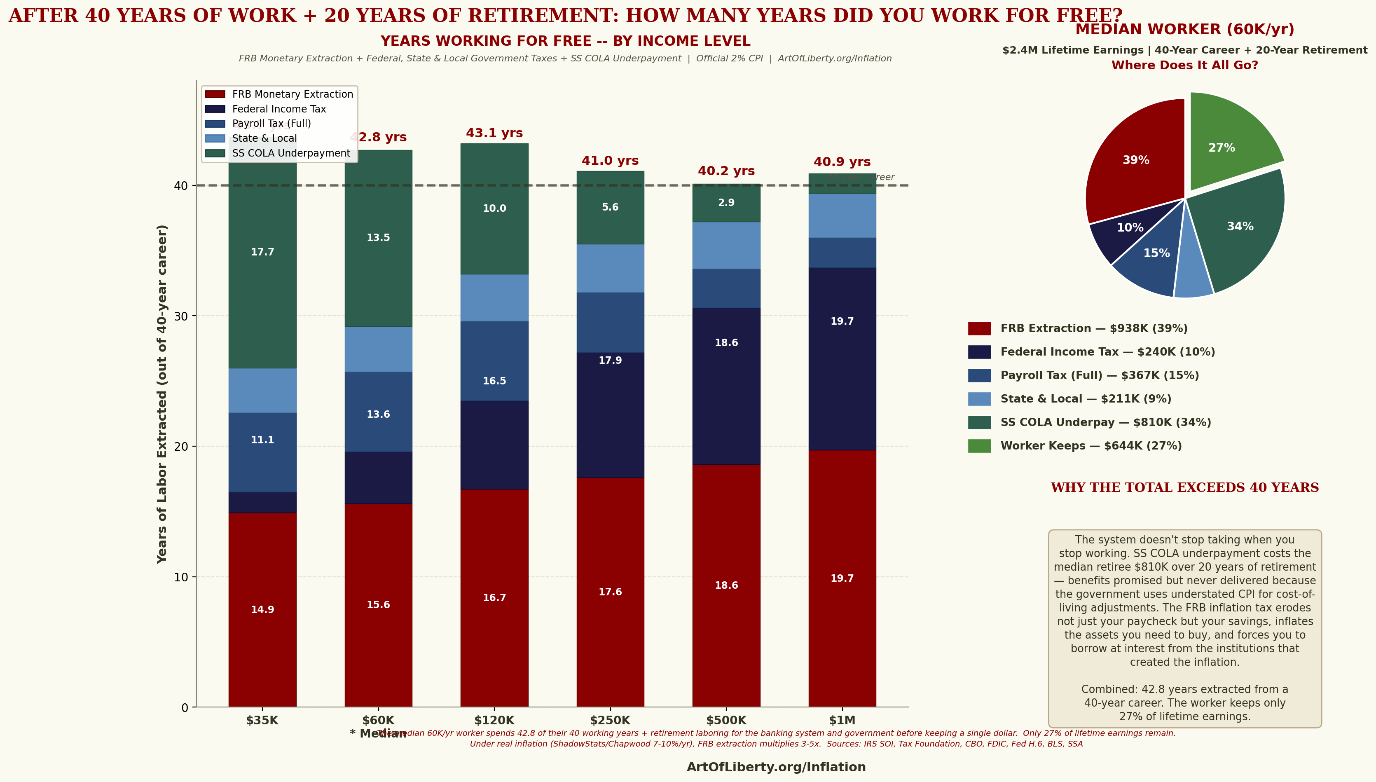

How Many Years Did You Work For Free?

Here is the clearest way to see the scale of the extraction. After a 40-year career and 20-year retirement, how many of those 60 years did you work just to cover the wealth transferred to the banking system, the government, and the CPI manipulation that reduces your retirement benefits?

For the median worker at $60K, the combined extraction represents 42.8 years of labor — more than the entire 40-year career. The worker keeps only 27% of lifetime earnings.

Every income level from $35K to $1M exceeds 40 years of extraction because of two dynamics:

1. Under an honest monetary system like the historical gold standard where dollars can't be created digitally or on a printing press, prices are benignly deflationary. The costs of the luxuries and necessities of life go DOWN each and every year 1-2% reflecting the innovations in better manufacturing, cheaper materials and more effective distribution. The average worker would be getting richer, the Cantillon Effect would be eliminated, and workers wouldn't have to borrow (Or would borrow much LESS for houses, education, and healthcare)

2. The SS COLA underpayment continues extracting value during retirement. The system doesn't stop taking when you stop working. The government continues stealing from you by underpaying you what you are due from mandatory Cost-Of-Living-Adjustments by lying about what the REAL rate of inflation is.

The extraction is most devastating for those who can least afford it. The $35K earner loses 17.7 years to SS COLA underpayment alone — 44% of lifetime earnings — while the $1M earner loses only 1.5 years to the same mechanism. The system is regressive by design.

This Is Not Accidental

The report documents five hallmarks of organized crime that sustain this extraction:

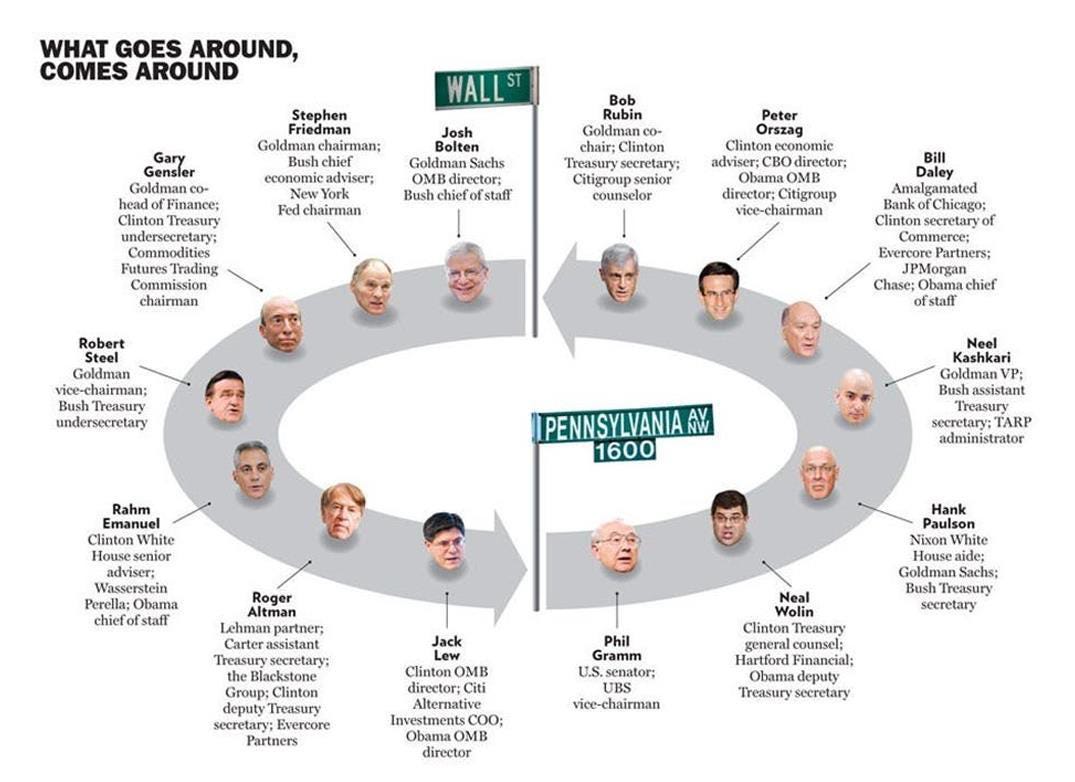

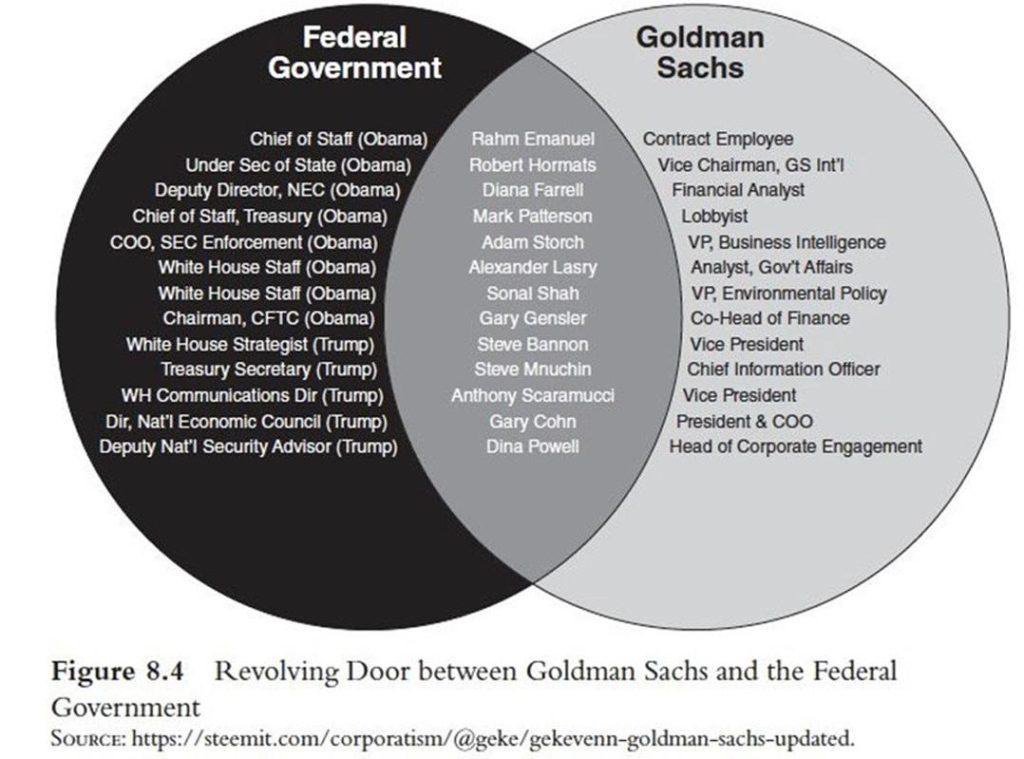

Regulatory Capture: 304 revolving-door hires between the 20 largest U.S. banks and regulatory agencies, representing 2,256 cumulative years of public office (Cambridge University Press / Journal of Institutional Economics, 2019).

Capture of the Economics Profession: The Federal Reserve spends hundreds of millions annually funding economists at universities, journals, and conferences. 84 of 190 editorial board members across top economics journals have Fed ties. The field cannot produce independent criticism of the institution funding it.

Capture of Government: The FIRE sector has been the largest or second-largest source of federal campaign contributions in nearly every election cycle since 1990, totaling over $20 billion since tracking began — producing a 180:1 return on political investment. Industry executives cycle in and out of government at the highest levels.

Capture of Academia: Compulsory schooling systems presents "government" as legitimate, desirable and necessary before kids are old enough to evaluate the logic and morality of the claim. The schools present the Federal Reserve as a neutral public institution, never teach that banks create money through lending, and never question or debate the legitimacy of the system.

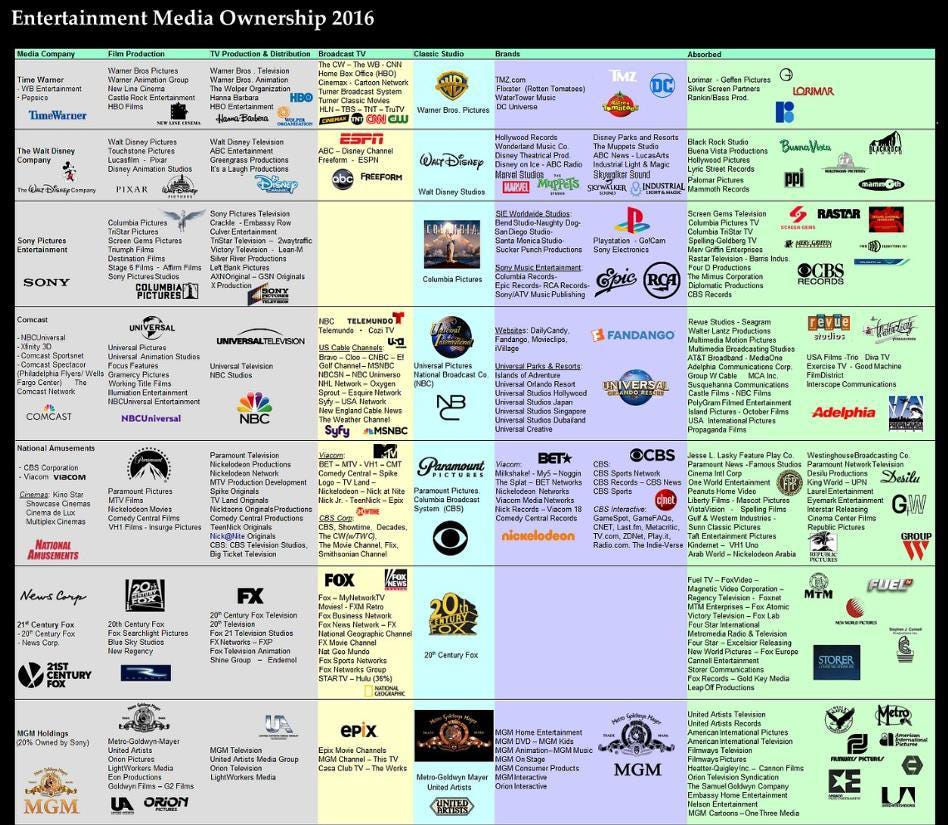

Monopolization of Media: Six corporations now control approximately 90% of what Americans see, hear, and read. The consolidation was financed with cheap debt from the very banking system being normalized. No major network has produced a serious investigative piece on fractional reserve banking as a mechanism of wealth transfer.

What You Can Do Right Now

First: verify it yourself. Open any AI model — Claude, Grok, Gemini, or ChatGPT — and ask it to calculate the lifetime cost of the fractional reserve banking system to a median worker at your income level. We have specific prompts in the report. You will get a number in the same range documented in this report. The directional transfer from wage-earners to money-creators is a consensus finding across every model tested.

Second: share this report. It is released under Creative Commons Attribution 4.0 — reproduce and distribute freely with attribution. You can download the full PDF with hyperlinks at ArtOfLiberty.org/Inflation. You can buy printed copies at ArtOfLiberty.org/Store.

Third: support the Art of Liberty Foundation! We are an independent organization with no government funding, no banking-sector advertising revenue, and no institutional dependencies. The work described in this report — and the investigative journalism that will follow — depends entirely on voluntary support. Become a sponsor at ArtOfLiberty.org/Sponsor.

"The magicians can only fool the audience until the audience understands the trick.

That moment is now."

— Etienne de la Boetie², Art of Liberty Foundation

Watch Streaming Broadcast Live:

LRN.fm

DLive

Telegram